export growth strenghtens

The 2025/2026 export season shows a further strengthening of the recovery that began last year. After two seasons of clear contraction, 2024/2025 already delivered a strong rebound. That upward trend is continuing this season. Up to and including week 19, exports reached more than 1.2 billion kilograms, around 9 percent higher than in the same period last year. The sector is therefore building further on last season’s recovery, although the composition of exports is changing significantly.

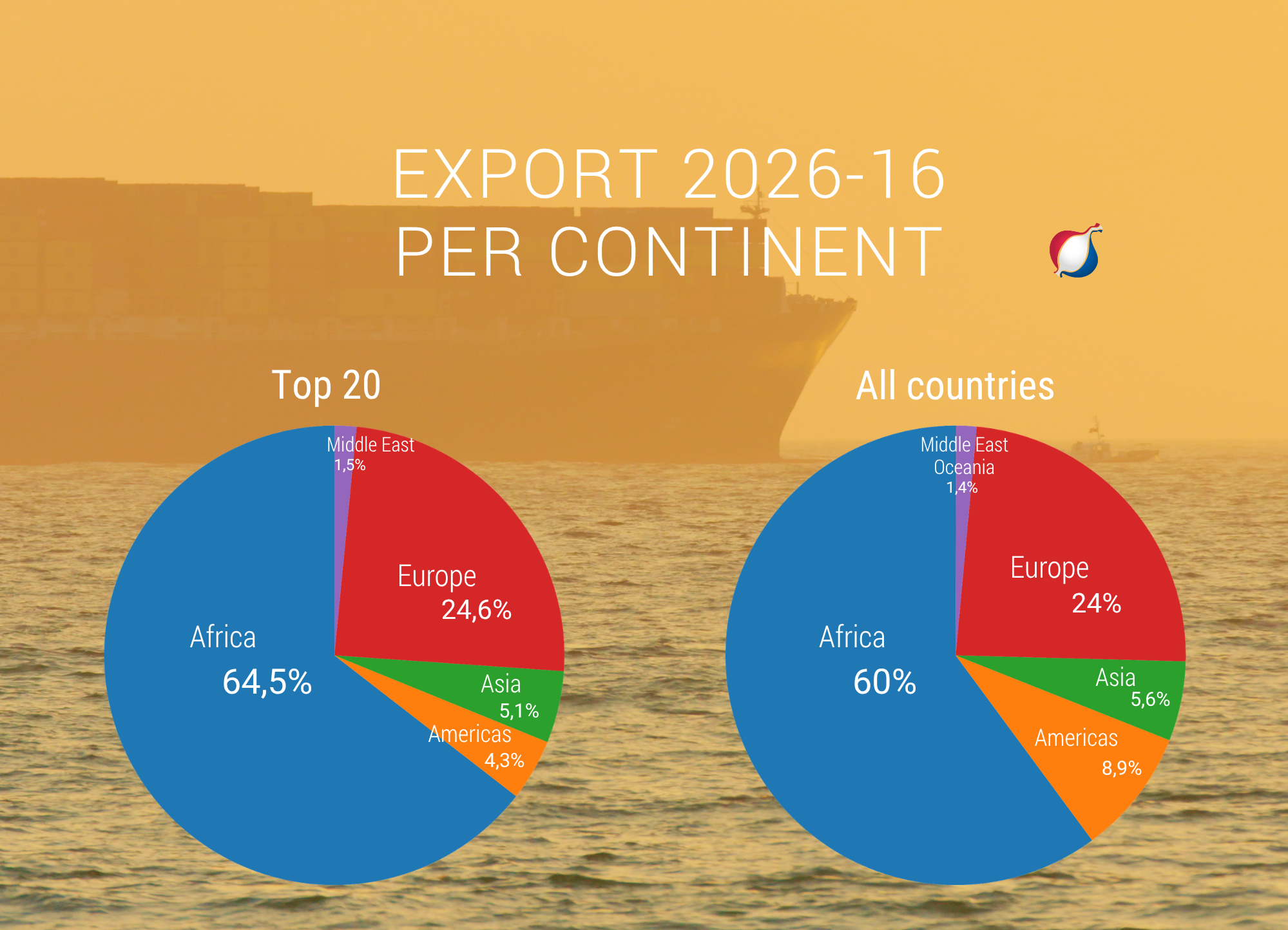

Africa confirms role as the main pillar market

As in previous years, West Africa forms the foundation of Dutch onion exports. This season, however, that dependence is greater than ever. More than 60 percent of total export volume is destined for this region. West Africa remains the main growth engine of Dutch onion exports, while Asia and the Americas are simultaneously becoming increasingly important as additional growth regions. This is creating a more international and geographically diversified export profile.

Senegal and Côte d’Ivoire dominate the picture in particular, supplemented by countries such as Guinea, Mali and Mauritania. The concentration within exports is remarkably high.

The two largest destinations account for a substantial share of total volume, while the top five countries together absorb the majority of exports. This underlines that this season’s growth is largely driven by a limited number of markets. At the same time, this structure makes the sector vulnerable. As soon as demand in one of these core markets weakens or slows, the impact on total export volume is immediate.

Europe loses ground, but shows a mixed picture

Europe is playing a noticeably smaller role this season compared with last year. Total export volume to European destinations is approximately 12 percent lower. Nevertheless, the picture within Europe is far from uniform. On the one hand, there are clear growth markets. The United Kingdom is showing strong growth of 40 percent, confirming its position as the most important European buyer. Ireland and Norway are also recording growth. On the other hand, several destinations have declined sharply. Belgium (-50 percent), France (-32 percent) and Poland (-96 percent) have all fallen back considerably. In Eastern Europe, weak demand is the main factor, while in Belgium and France trade flows and timing also play a role. The result is a polarised picture: Europe is not so much a shrinking market as a region where demand is increasingly concentrated in a limited number of countries.

Harvests determine the direction of trade

The differences between European destinations can largely be explained by the 2025 harvest situation. The Netherlands experienced an exceptionally good year, with a record crop of approximately 1.7 million tonnes (+17 percent). This is creating substantial export pressure. Other European countries show a more mixed picture. Germany also achieved a strong harvest (+21 percent), further reducing its dependence on imports. Decades ago, Germany was still one of the key export markets for Dutch onions, but it is increasingly moving towards self-sufficiency. German growers are even becoming increasingly important suppliers for Dutch onion traders.

Spain, by contrast, saw production decline by around 10 percent. In addition, Spain is normally a major competitor in the UK market, where Dutch onions are now filling demand and gaining market share. France struggled with storage quality issues, although this has not yet translated into a clear increase in imports. Overall, there is no broad European shortage this season. The market is being driven more by the large Dutch supply than by structural shortages elsewhere in Europe.

Seasonal pattern follows familiar course

The season is largely following its familiar pattern. In the initial phase, European destinations briefly dominate, after which West Africa quickly takes over and export volumes rise sharply. Around week 10, a transition phase begins, during which African demand weakens as local short-day onion harvests become available and other markets start to emerge. That transition is currently visible. However, the shift towards alternative markets is less pronounced than in some previous seasons. The Middle East in particular is lagging behind, as exports to Israel are significantly lower than last year. Despite rapid interventions from both trade and government aimed at keeping the market open, this has not yet resulted in higher volumes. At the same time, European markets are cautiously beginning to return.

Asia and the Americas grow as additional sales markets

The most striking development outside Africa is the strong growth towards Asia and the Americas. Although these regions remain smaller in absolute terms, together they account for a substantial share of total export growth. Asia is showing clear growth, with countries such as Malaysia, the Philippines and Japan importing higher volumes. Although the market share remains relatively modest, the strong growth points to structural opportunities. Sales to Central and South America are also increasing. Countries such as the Dominican Republic, Nicaragua and Honduras are increasingly functioning as supplementary markets, particularly during periods when Africa is less dominant. Dutch onions were even exported to Cuba this season. This development contributes to a broader spreading of risks.

Growth towards markets such as Morocco and Brazil is linked to climate and harvest problems in those countries. Morocco has struggled with persistent drought and disappointing harvests in recent seasons, temporarily driving up import demand. Brazil is normally largely self-sufficient in onions, but in periods of regional shortages, logistical disruptions or disappointing harvests, the country traditionally turns to Dutch onions on a regular basis. The Netherlands plays an important global role as a reliable and flexible exporter capable of supplying volumes quickly whenever shortages arise elsewhere.

Shipping disruptions

Disruptions in shipping around the Red Sea have created a structurally altered logistical situation since late 2023. Major container shipping companies are avoiding the Suez Canal route and instead sailing around the Cape of Good Hope, resulting in longer transit times, higher costs and less efficient use of capacity. Contrary to the perception of an oversupply of empty containers, market reality points more towards scarcity and uncertainty within the logistics chain. The fact that Dutch onion exports are nevertheless continuing to grow — while still serving distant markets such as the Philippines and Japan — underlines the strong demand and flexibility of the sector.

Worldwide distribution reaching even the smallest markets

Dutch onion exports are characterised by an exceptionally broad geographical spread representing around two-thirds of all countries worldwide. Up to and including week 19, a total of 130 countries had been supplied. This gives the Netherlands one of the most extensive export networks within the international onion trade. Remarkably, Dutch onions find their way not only to major sales markets, but also to a range of more unusual destinations. These include the Seychelles, Antigua and Barbuda, Barbados and the Bahamas, as well as smaller markets such as Belize, Brunei and Bahrain. Trading hubs such as Hong Kong are also part of this network. These “exotic” destinations illustrate the exceptional flexibility and global reach of the Dutch onion sector.

When the analysis is expanded from the top 20 destinations to all markets, the truly global nature of Dutch onion exports becomes even clearer. Although Africa remains dominant in terms of volume, its relative share declines as more smaller markets are included. The Americas and Asia then gain further importance.

Recovery with a new dynamic

Dutch onion exports are once again showing convincing recovery this season, but the underlying dynamics are changing. While growth in volume is positive, dependence on West Africa is simultaneously increasing further. At the same time, Europe’s role is shifting from bulk buyer to a more selective market. The sector is therefore entering a new phase in which flexibility, risk diversification, logistical strength and market expertise are becoming increasingly important.

This season’s growth inspires confidence, but also demonstrates that the structure of international sales markets is changing faster than before.